An income statement is one of the three main financial reports for your company. It holds vital information about your business such as revenue and expenses – painting a clear picture of the company’s profitability and operational efficiency over a specific period. This document serves as an essential tool for business owners, investors, and financial advisors to assess financial performance and make informed strategic decisions.

Let’s unpack the details of the income statement, including what it is, its importance and how to successfully prepare one.

What is an income statement?

An income statement, also known as a profit and loss statement, is a fundamental financial document that provides a snapshot of a company’s financial performance over a specific period. This statement records all revenues and expenses of the business, ultimately revealing the net profit or loss incurred.

What does an income statement look like?

An income statement consists of revenue, expenses and profits. Each section holds different line items that will convey the money earned (revenue), the money spent (expenses) and how much of the money you retained (profits.)

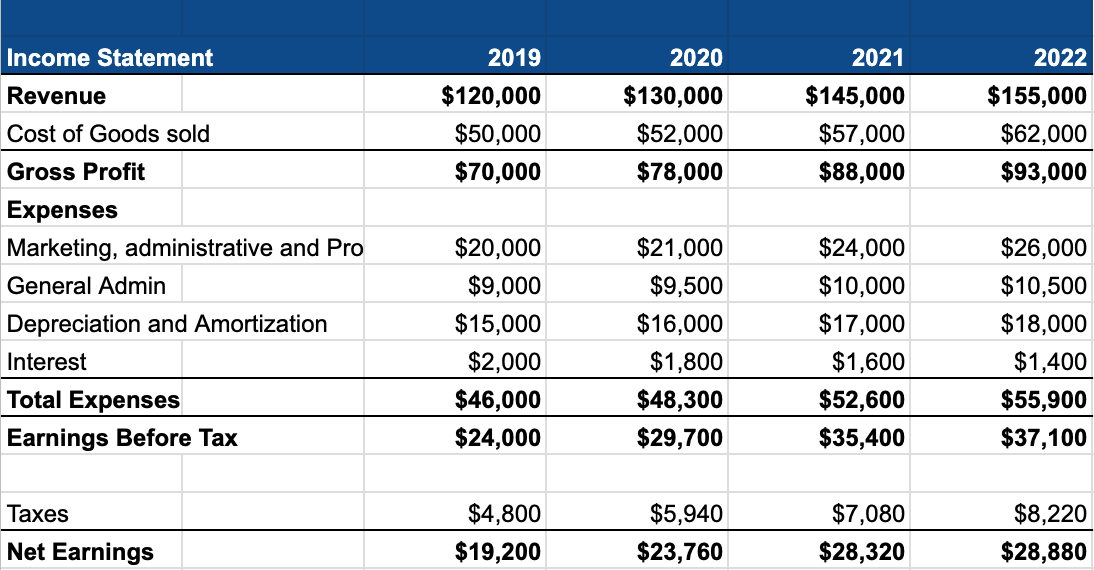

See the image below for an example of what a simple income statement would look like.

Source: Swoop Funding.com

What does an income statement include?

Every company is different and will prepare their income statement depending on their industry and business accounting practices. But the main components of an income statement should be similar to the following:

- Sales or revenue

- Cost of goods sold (COGS)

- Gross profit

- Operating expenses

- Earnings before tax

- Net income or loss

Sales or revenue

Sales or revenue is the income received by a company from its business activities, typically from the sale of goods and services to customers. It is the starting point of an income statement and serves as an indicator of a company’s potential to generate profit. High revenue, however, does not always equate to profitability, as expenses must also be taken into account.

Example:

A financial advisor’s income from asset management fees, which are charged based on a percentage of the client’s assets under management, would be recorded as sales or revenue on the income statement. Similarly, a broker’s commission from executing trades on behalf of a client would also fall under this category.

Cost of goods sold (COGS)

Cost of Goods Sold (COGS) represents the direct costs attributable to the production of the goods sold by a company. This includes the cost of the materials and labor directly used to create the product. COGS is deducted from revenues to determine the gross profit of a business.

Example:

For a financial broker offering mutual funds, any direct costs paid to fund managers for selecting the portfolio of the fund can be considered as COGS and would be recorded as such on their income statement.

Gross profit

Gross profit is the income a company has left over after deducting the costs associated with producing and selling its products, known as COGS. It is a crucial indicator of a company’s manufacturing and distribution efficiency and serves as a key figure from which to pay expenses, invest in product development, and generate net income.

Example:

If an advisor charges $10,000 for financial planning services and incurs $2,000 in direct costs to deliver these services, the gross profit recorded would be $8,000.

Operating expenses

Operating expenses are the costs associated with running a company’s day-to-day operations that are not directly tied to production. These expenses include rent, utilities, salaries for administrative staff, and marketing costs. Managing operating expenses is vital for maintaining profitability.

Example:

The cost of leasing office space, salaries of support staff, and marketing for a financial advisory firm are operating expenses and would be deducted from the gross profit on the income statement.

Earnings before tax

Earnings before tax (EBT) is a measure of a company’s financial performance that calculates the profit made before taxes are applied. It includes all profits from operations and deducts all expenses including interest. EBT provides insight into a company’s ability to generate profit from its core business before the impact of the tax regime.

Example:

A broker’s earnings from trading commissions, after all operating expenses and interest on business loans are deducted but before taxes, would constitute their EBT.

Net income or loss

Net income or loss is the final amount of profit or deficit after all expenses, including taxes and interest, have been subtracted from total revenues. It is the most telling figure of a company’s financial health over a reporting period, reflecting its ability to turn revenue into profit effectively.

Example:

After a financial advisor pays all operational costs and taxes out of their earnings from client fees, the remaining amount is the net income and is what the advisor actually earns from their business activities. This is the figure that would be reinvested into the business or distributed to shareholders.

How to prepare an income statement

Preparing an income statement correctly involves a number of steps that integrate with the logical flow of calculations as well as promotes accuracy. Beyond this, keeping with this order also ensures that you can stay in compliance with accounting standards, as both Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) have specific requirements regarding the presentation of financial statements.

Here are the nine steps to preparing an income statement.

Step 1: Pick a timeframe to report on

The decision on the timeframe is typically driven by the business cycle, regulatory requirements, and management needs. An ideal timeframe for most businesses is quarterly or annually, as it allows for both short-term operational analysis and long-term strategic planning. Staying on schedule with regular reporting periods ensures consistency and comparability in financial reporting.

For a financial broker, maintaining a consistent reporting schedule can significantly aid in tracking commission income patterns and client investment behaviors, which can inform more strategic advising. For example, a broker who reviews their income statement quarterly is better positioned to adjust their business strategies promptly to respond to market changes or client needs. Conversely, not staying on schedule may lead to missed opportunities for optimization or delayed recognition of critical financial issues, which could result in suboptimal advice, client dissatisfaction, or financial losses.

Step 2: Calculate total revenue

Total revenue is calculated by summing up all the income generated from the business’s primary operations during the reporting period. It includes earnings from sales of goods or services, interest received, dividends, and any other income directly resulting from the core business activities. Accurately calculating revenue ensures that the income statement reflects genuine business activity, crucial for assessing the business’s performance and making informed strategic decisions.

Keep in mind that revenue does not include loans or capital infusions, which are not earned but rather borrowed or invested capital.

Calculating total revenue for a financial advisor might be calculating total revenue by adding up all the fees earned from financial planning services, commissions from selling financial products, and any performance-based bonuses over the quarter.

On the other hand, suppose an advisor received a capital investment to expand their operations. In that case, this amount would not be considered part of the revenue, as it is not generated from the advisor’s services but is rather a contribution to the capital of the business.

Step 3: Calculate total COGS

The calculation of Total Cost of Goods Sold (COGS) involves tallying all direct expenses associated with the production of goods or services that a company sells. COGS should include direct labor costs, raw materials, and manufacturing overhead. It does not encompass indirect expenses such as distribution costs, sales force costs, or advertising expenses.

For service-oriented businesses like financial brokerage, COGS might encompass direct costs such as transaction fees or purchase costs of financial products that are passed on to clients.

Step 4: Calculate gross profit

Gross profit is determined by subtracting the total COGS from the total revenue. It measures the efficiency of a company in managing its labor and supplies in the production process. Gross profit focuses solely on the relationship between the cost of goods sold and the revenue generated from those goods, not including operating expenses, taxes, or other costs.

For a financial broker, gross profit would be the difference between the revenue generated from client transactions and the direct costs associated with executing those transactions. If a broker generates $50,000 in commissions and incurs $10,000 in direct trading fees, the gross profit would be $40,000. This figure is critical as it represents the core profitability of the brokerage services before any other costs are accounted for.

Step 5: Calculate operating expenses

Operating expenses encompass all costs required to operate the business that are not directly tied to the production of goods or services. This includes rent, utilities, salaries for non-production staff, marketing, and professional fees. These are subtracted from the gross profit to determine the operating income.

A financial advisor’s operating expenses might include office rent, salaries for administrative staff, marketing costs, and subscription fees for market analysis software. If the total operating expenses for the period are $15,000 and the gross profit is $40,000, the remaining amount would be the income from operations, which, in this case, would be $25,000.

Step 6: Calculate income

Income, often referred to as operating income or earnings before interest and taxes (EBIT), is the profit from normal business operations. It’s calculated after subtracting operating expenses from the gross profit. This figure does not include any profits or losses from non-operating activities, interest payments, or taxes.

For brokers, operating income would be the net amount earned after all costs of conducting day-to-day business are covered. Using the previous example, with a gross profit of $40,000 and operating expenses of $15,000, the operating income would be $25,000.

Step 7: Calculate interest and taxes

Interest expenses incurred on debts and taxes due to the government must be considered to arrive at the net income. Interest is calculated based on outstanding loans, while taxes are computed according to applicable tax rates and regulations. These figures are subtracted from the operating income.

A financial advisor may have a business loan with a yearly interest expense of $5,000 and an estimated tax obligation of $7,000 for the year. These amounts would be deducted from the operating income to determine the earnings before tax and, subsequently, the net income after taxes.

Step 8: Calculate net income

Net income is the final line of the income statement and represents the total profit or loss after all expenses, including interest and taxes, are subtracted from revenue. It is the amount the business has earned or lost during the reporting period.

If a broker’s operating income is $25,000, with interest and taxes totaling $12,000, the net income would be $13,000. This is the final profit figure and represents the financial success of the brokerage over the reporting period.

Step 9: Finalize the document

Finalizing the income statement involves ensuring all numbers are accurate and appropriately formatted. The document should be clear, easy to understand, and compliant with the generally accepted accounting principles (GAAP) or other relevant standards.

For financial advisors, finalizing the income statement might include reviewing the document for accuracy, ensuring that it aligns with compliance requirements, and possibly having it reviewed by a certified accountant. An accurate and well-presented income statement can be a valuable tool for assessing business performance and making strategic decisions.

How Swoop can help

With our advanced finance-matching and deal flow management capabilities, Swoop is uniquely positioned to partner with you in discovering the most fitting funding solutions across debt, equity, and grants. Our platform is designed to identify and facilitate substantial savings, enhancing your value to your clients.

In this fast-paced environment, let the intricate details of sourcing and managing funding be a concern you delegate to us. Swoop Funding stands ready to streamline this process, allowing you to focus more on the core operations of your business. Our commitment is to make you indispensable to your clients by simplifying the complexities of funding and savings opportunities.

With Swoop, you gain a trusted ally, empowering you to channel your efforts into what you do best: guiding your clients towards financial growth and stability. Let your business operations be the bulk of your concern, and leave the intricacies of funding and financial optimization to us – we’re here to ensure you and your clients thrive.

yet? Register here!

yet? Register here!