Understanding the dynamics of credit scores can often feel like navigating through a maze, with each turn influenced by various financial decisions and behaviours. For financial advisors and brokers, you’re expected to demystify this journey for your clients, providing them with the clarity and guidance needed to maintain or improve their financial health.

Here at Swoop, we recognise the importance of a healthy credit score in securing loans and funding options. We’ll help identify the common reasons behind a drop in credit scores, underscoring the pivotal role such insights play in crafting effective investment strategies. Through Swoop Funding’s lens, we aim to illuminate the path for finance professionals, enabling them to leverage our platform’s unique opportunities to benefit their clients.

Let’s unpack the factors that can influence credit score fluctuations and how understanding these can be a game-changer in the financial landscape.

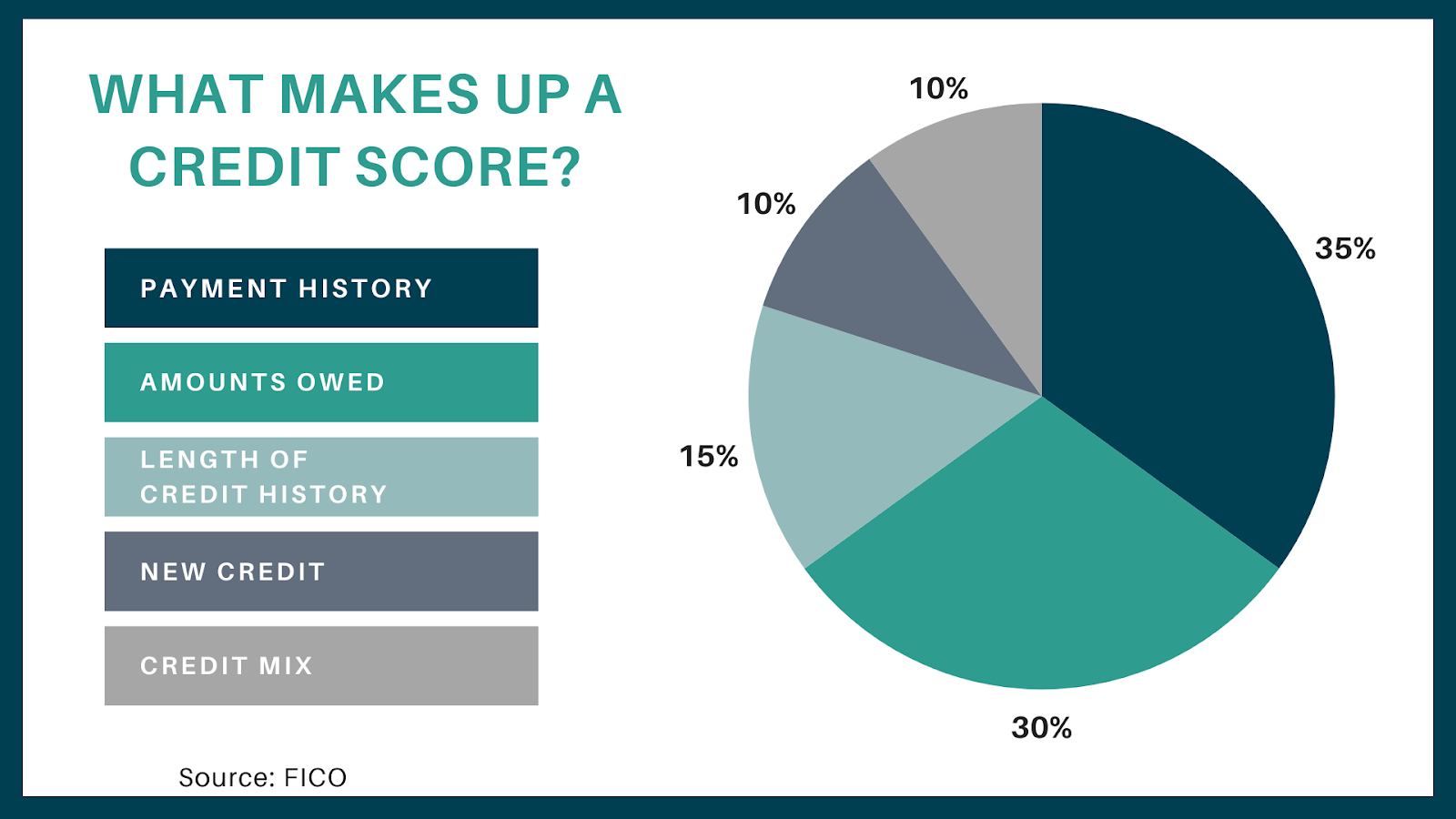

What makes up your credit score?

Your credit score is composed of five separate categories with different weights. Some affect your score more than others.

- Payment history (35%)

- Amounts owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

Alt text: pie-chart-showing-the-five-FICO-scoring-categories-and-percentages

6 Reasons why your credit score has dropped

A credit score is a dynamic metric that reflects your financial reliability. Its fluctuations can impact your ability to access various financial products. For clients navigating the complexities of their financial journey, understanding the reasons behind a credit score decline is crucial.

This knowledge not only empowers them but also enables financial advisors and brokers to provide targeted advice and solutions. We will explore the following common factors contributing to a decrease in credit scores:

- You have late or missing payments

- You recently applied for a mortgage, loan, or new credit card

- Your credit utilisation has increased

- One of your credit limits decreased

- You closed a credit card

- There is inaccurate information on your credit report

1. You have late or missing payments

Implications: Payment history is a large component of your credit score (35%). Late payments not only reflect poorly on your financial responsibility but also signal risk to future lenders. The impact of a late payment can vary based on how late the payment is, how often you’ve been late, and how recent the late payment was.

Practical Steps: Set up automatic payments for regular bills to avoid oversight. If you face financial hardship, contact your creditors before a missed or late payment to discuss possible adjustments to your payment schedule or temporary relief options. Making a payment before 30 days past due can prevent it from being reported to the credit bureaus.

2. You recently applied for a mortgage, loan, or new credit card

Implications: Each hard inquiry from a credit application can slightly reduce your credit score. The hit of a “new credit inquiry” can stay on your profile for two years before no longer showing as new. The rationale is that seeking new credit could indicate financial instability or an increased risk that you will overextend yourself.

Practical Steps: Only apply for new credit when necessary. Use lenders’ pre-approval processes to gauge your eligibility for credit cards or loans without impacting your credit score. Space out applications every two years if possible to minimise the cumulative impact of hard inquiries. This includes auto loans, personal loans, and credit cards.

3. Your credit utilisation has increased

Implications: Credit utilisation—how much credit you’re using compared to your total available credit—is also a pivotal factor, illustrating your dependency on credit. A sudden spike in utilisation can alarm creditors, suggesting a change in your financial stability or risk profile.

Practical Steps: Pay more than the minimum payment on credit cards to gradually reduce balances. If possible, make multiple payments throughout the month to keep balances low. Monitor your credit card statements closely and adjust your spending habits to keep utilisation in check.

4. One of your credit limits decreased

Implications: Creditors may lower credit limits based on their risk assessment, which can unfavourably affect your credit utilisation ratio. Sometimes, this happens without warning and for reasons outside your direct financial behaviour, such as economic downturns or changes in the lender’s policies.

Practical Steps: Regularly review your credit limits and speak with your creditors if you notice a decrease. Maintaining a good relationship with them and demonstrating financial stability can sometimes persuade them to reconsider their decision. Alternatively, paying down balances can help manage your utilisation ratio.

5. You closed a credit card

Implications: The rule of thumb is to never close a credit card because it hurts more than it helps. Closing a credit card account reduces your overall available credit and can shorten your credit history, particularly if you close an old account. This can inadvertently increase your credit utilisation ratio and remove a history of on-time payments from your credit report.

Practical Steps: If you must close an account, try to pay down balances on other cards to mitigate the impact on your utilisation ratio. Also, keep an eye on credit cards you haven’t used in a while, the issuer may close your account for you which can have the same effect as closing a card yourself.

6. There is inaccurate information on your credit report

Implications: Errors on your credit report, such as incorrect late payments, fraudulent accounts, or identity theft, can unjustifiably lower your credit score. These inaccuracies can stem from clerical errors, misreported information, or more sinister activities like fraud.

Practical Steps: Review your credit reports regularly from major credit bureaus. If you find inaccuracies, file disputes with each bureau online or by mail, providing documentation to support your claim. Follow up on your disputes to ensure corrections are made.

What is considered a good or bad credit score?

Generally, good credit is anything over 700. Average credit is between 600 and 700, anything below 600 is poor but this can vary.

- A score of 670 to 739 is considered “good,” indicating a borrower that lenders are likely to view as dependable.

- Scores from 740 to 799 are deemed “very good,” showing better lending terms and lower interest rates are likely.

- A score of 800 and above falls into the “exceptional” category, which can lead to the most favourable borrowing terms.

A credit score below 670 begins to enter the “fair” or even “poor” categories, which can make it more difficult to qualify for favourable credit terms. Scores in these lower ranges might lead to higher interest rates or the need for a co-signer when applying for loans.

How to improve your credit score

Improving your credit score is a strategic process that requires consistent effort and financial discipline. By understanding the factors that influence your credit score, you can take targeted actions to enhance it. Here are key strategies to consider:

- Pay your bills on time: Your payment history is a significant factor in your credit score. Late payments can negatively affect your score, so ensure you pay all your bills, including credit cards, loans, and utilities, on time. Setting up automatic payments or reminders can help you stay on track.

- Reduce your credit utilisation ratio: This ratio measures how much of your available credit you’re using and is a critical factor in credit scoring models. It’s recommended to keep your credit utilisation below 30% of your total credit limit. You can achieve this by paying down existing balances and avoiding large purchases on credit.

- Keep old credit accounts open: The length of your credit history contributes to your credit score. By keeping older accounts open and active, you demonstrate a longer history of responsible credit use. Closing old accounts can shorten your credit history and potentially lower your score.

- Limit new credit inquiries: Every time you apply for a new line of credit, a hard inquiry is made to your credit report, which can temporarily lower your score. Limit the number of new credit applications, especially within a short time frame, to avoid negative impacts.

- Diversify your credit mix: Having a mix of credit types (e.g., credit cards, auto loans, and mortgages) can positively affect your score, as it shows you can manage different types of credit responsibly. However, it’s not advisable to take on new credit unnecessarily, just to improve your credit mix.

- Check your credit reports for errors: Inaccuracies on your credit reports can negatively impact your score. Regularly review your reports from major credit bureaus for any errors or discrepancies and dispute them promptly to have them corrected.

- Seek professional help if needed: If you’re struggling to manage your debt or improve your credit score, consider consulting with a reputable credit counselling service. They can offer personalised advice and help you develop a plan to improve your financial situation.

How Swoop can help

Throughout this article, we’ve explored the dynamics of credit scores, their impact on financial opportunities, and strategies for improvement. For financial advisors and brokers, integrating Swoop Funding into your toolkit can significantly enhance your ability to support clients in these areas.

Swoop offers innovative financial solutions, from loans to savings options, tailored to protect and grow businesses. By leveraging our smart matching technology and accessing expert advice, you can navigate the complexities of finance with confidence. Hit the “get started” tab and unlock these opportunities to help drive your clients towards financial success.

yet? Register here!

yet? Register here!